The 5 Signs Your Brand is Costing You Your Series A

Most early-stage companies don't fail because the technology isn't real. They fail because no one important understands it fast enough. At Seed, you can survive that. At Series A, you can't.

WHY THIS MATTERS NOW

The Series A window has never been harder to hit.

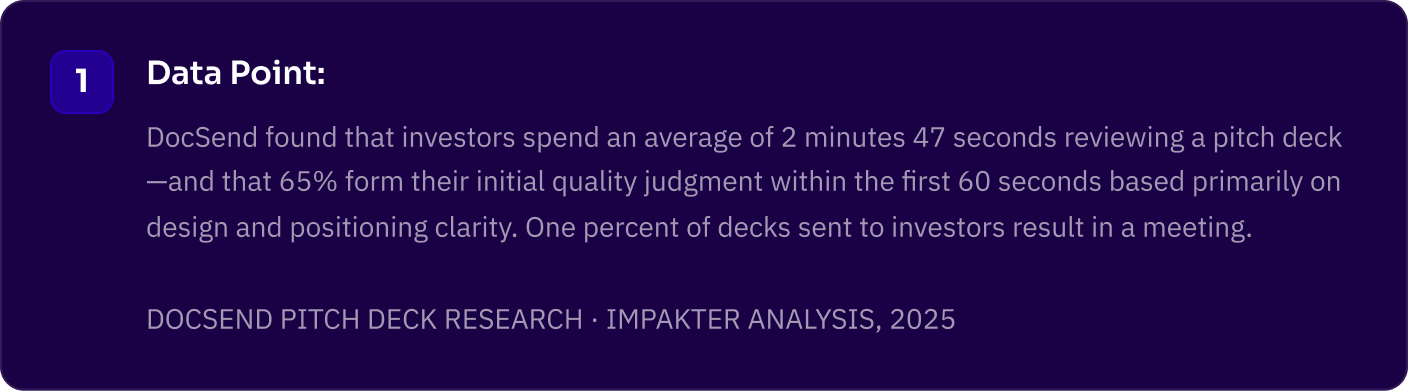

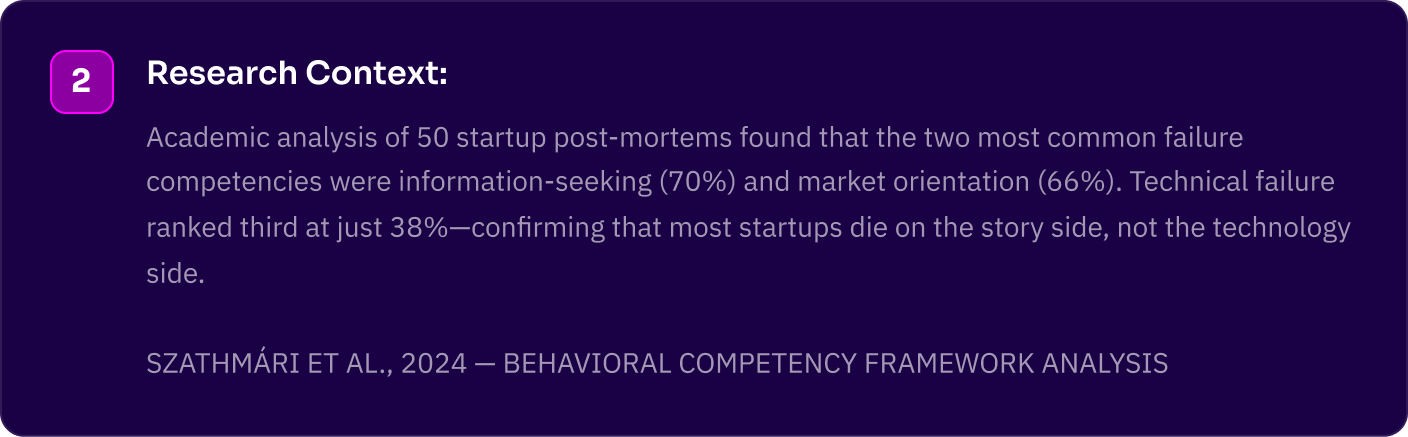

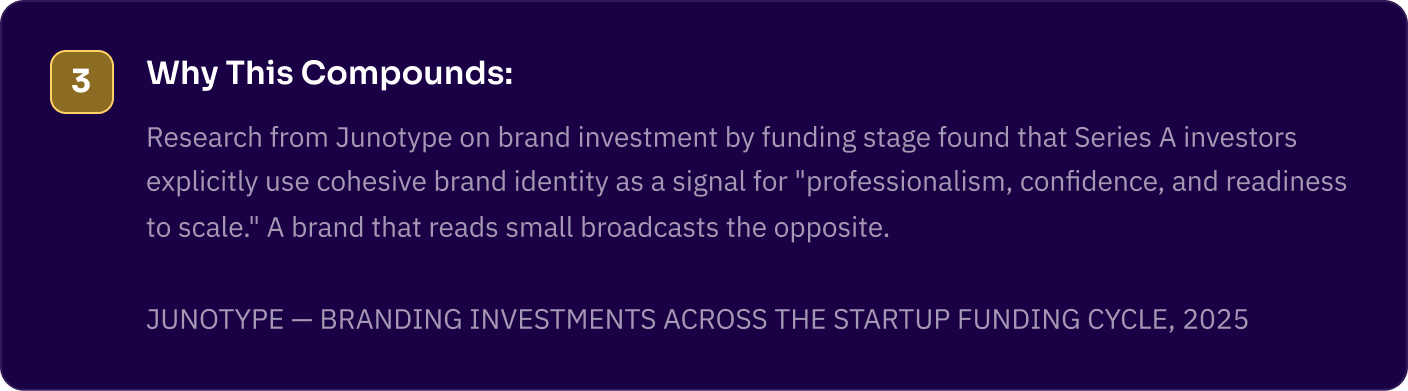

The conversion rate from seed to Series A has collapsed. In 2018, roughly 30% of seed-funded startups graduated to a Series A within two years. By early 2022, that number was 15.4%—a near 50% drop. For SaaS companies specifically, it fell from 37% to just 12%.

The capital is still out there. AI startups claimed 31% of all global VC funding in Q3 2024. The average Series A round is now $16.6 million. But the winners are fewer, and the bar to get there has fundamentally shifted.

Here's what hasn't changed: investors still evaluate you the same way they always have—through pattern recognition, fast categorization, and risk pricing. And what makes that harder now isn't the complexity of your technology. It's whether your story translates fast enough to survive first contact.

This is where brand stops being aesthetic and becomes infrastructure. Not your logo. Not your color palette. Your positioning—the layer that determines whether sophisticated investors can rapidly understand, categorize, and price risk against what you've built.

The founders who lose their Series A rarely lose it because the tech isn't compelling. They lose it because the story around the tech doesn't land in the window they're given. Here are the five signs that's happening to you.

THE FIVE SIGNALS

What investors are actually telling you.

Sign 01

Investors "like it" but don't move forward.

You've had the meetings. The response is warm. You're collecting variations on the same non-answer:

"Super interesting.""Come back when you have more traction.""Still wrapping our heads around it."

That last one is the tell. Investors don't pass because your technology is hard to understand. They pass because your positioning doesn't give them a fast mental model to work with. And without a fast mental model, they can't price risk. And if they can't price risk, they don't write checks.

Categorization is the prerequisite to investment. Before an investor can evaluate your traction, your market, or your team, they need to know what you are. If that question takes more than a minute to answer, the friction accumulates—and polite ambiguity becomes a pattern.

Sign 02

You're constantly re-explaining what you do.

Every conversation starts from zero. You're reframing the company in every pitch. Adjusting language depending on the audience. Explaining the same concept five different ways and still not sure any of them landed.

This isn't a communication problem. It's a positioning problem.

The re-explaining loop is a symptom of not having a stable positioning layer, a single, defensible answer to "what are you and why does it matter" that holds across contexts. Strong companies don't explain differently. They translate consistently. The core never changes; the framing adapts.

If you're rebuilding your story from scratch every time you walk into a room, you're asking each individual conversation to do the work that positioning should have already done. That's an expensive habit at Series A, where signal consistency is one of the data points investors are quietly tracking across every touchpoint they have with your company.

Sign 03

Your competitors sound exactly like you.

Scan the competitive landscape in any deep tech or AI vertical right now. The language is nearly identical:

"AI-powered platform", "Next-generation infrastructure","End-to-end solution", "Transformative technology"

These phrases are positioning voids. They describe a category of ambition, not a specific company. And when your differentiation only becomes visible after ten minutes of technical explanation, you've already lost the frame.

Series A investors fund clear, defensible categories. Not nuance. Not "we're like X but with Y added." They need to be able to answer the question their LP will ask: what does this company own, and why is that hard to replicate? If the answer to that question lives only inside your technical architecture and not in your positioning, it doesn't count yet.

Sign 04

Your website doesn't match your ambition.

You're building infrastructure. You're solving a category-level problem. In the room, that vision is unmistakable. Then an investor opens your website and reads something that sounds like a point-solution tool.

This mismatch is more damaging than founders typically realize, because investors use every touchpoint they have with your company as diligence data. Your website isn't just marketing. It's the first version of your story that investors encounter without you in the room to contextualize it and they encounter it before the meeting, not after.

When the ambient perception you're creating doesn't match the magnitude of what you're pitching, the delta reads as a credibility gap. The pitch becomes something to explain away rather than something to expand on. And at Series A, you want every surface working for you, not creating re-entry friction every time someone looks you up.

Sign 05

Your story breaks across audiences.

You're selling to technical buyers. Business stakeholders. Investors. And each one is hearing a different version of your company. The technical buyer gets the architecture. The business stakeholder gets the workflow. The investor gets something in between, calibrated in real time.

This isn't personalization. It's fragmentation. And investors sense it—especially the ones who've already spoken to your customers, read your website, and then walked into a pitch where the story felt like a different company.

The fix isn't simplification. It's architecture. Winning companies build one positioning foundation and multiple precise translations. The core claim stays constant—the frame, vocabulary, and proof points shift by audience. When that architecture is absent, every conversation you have with the market is making a slightly different deposit in slightly different accounts. None of them accumulate the way a single coherent brand does.

WHAT’S ACTUALLY HAPPENING

You don't have a brand problem. You have a translation problem.

You've built something technically sophisticated. The architecture is defensible. The moat is real. But the way it's communicated doesn't anchor to a clear category, doesn't map to buyer priorities, and doesn't scale across the conversations you need to have.

That gap has always existed between what founders build and what markets understand. What's changed is the cost of leaving it open. At Seed, ambiguity is acceptable—investors are funding a thesis. At Series A, they're funding a business they need to be able to explain to their partners in forty words or less. If you can't give them that, you're making their job harder than it needs to be.

The company that raises isn't always the most technically impressive one in the room. It's often the one whose story is the most investable—clear, differentiated, repeatable across every surface an investor touches on their way to a decision.

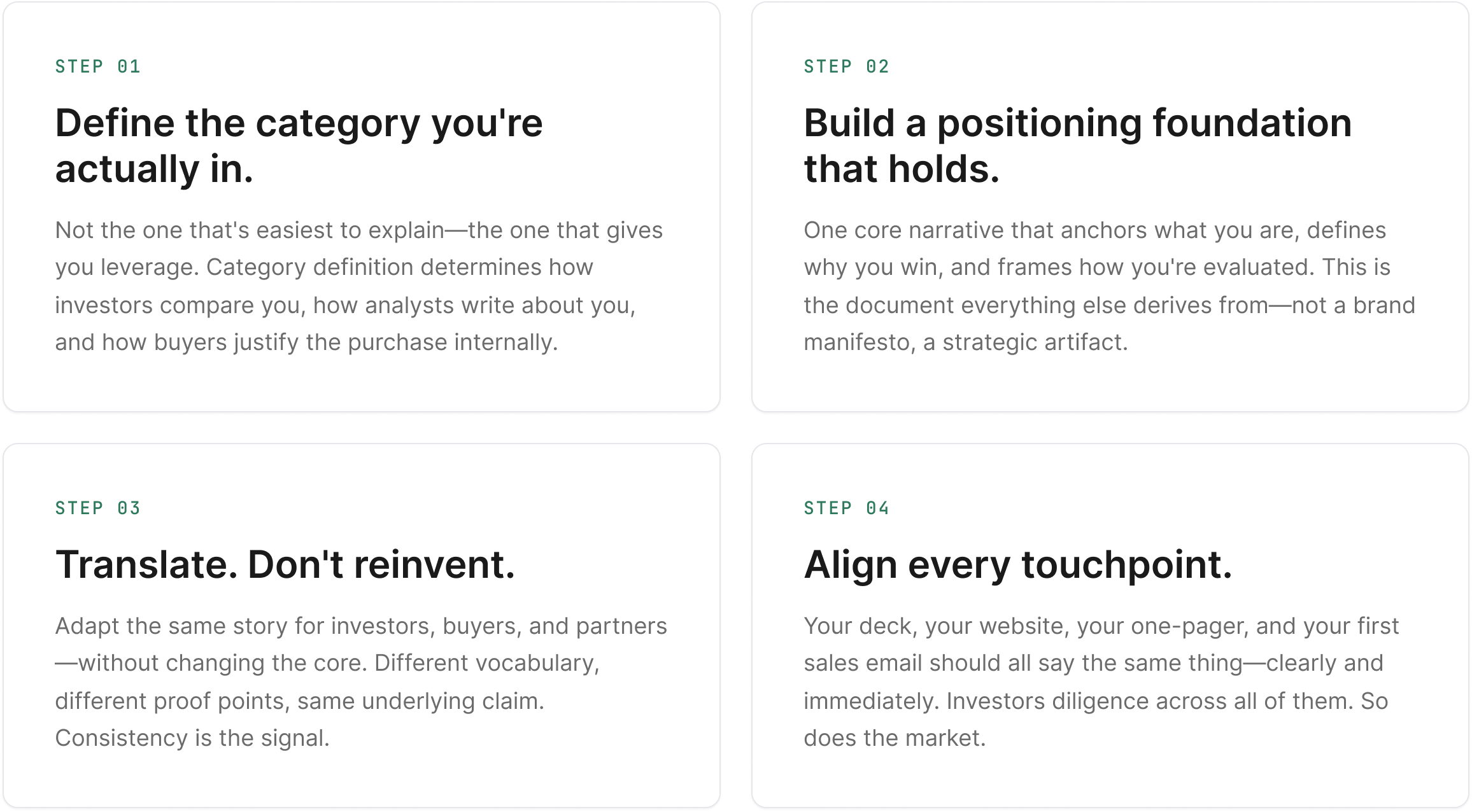

HOW TO FIX IT

Four moves. One foundation.

None of this requires a rebrand. It requires strategic clarity—executed all the way through.

THE BOTTOM LINE

Series A isn't just about proving the business.

It's about proving that the market can understand the business. Because if they can't understand it, they can't fund it. And if they can't fund it fast—inside the window you've been given, across every surface they check—the friction compounds into a pass.

The companies that raise in this environment don't have better technology than the ones that don't. They have a story that survives the room. A positioning layer that makes investors feel certain instead of cautious. A brand that looks as serious as the problem they're solving.

That's not a creative deliverable. That's infrastructure. And at Series A, it's the gap between a term sheet and another "super interesting."

Invisible Engine — Post-Seed Brand Strategy

If any of this feels familiar,

it's already costing you.

We work with frontier companies in the pre-Seed, post-Seed, pre-Series A window—where the story you build defines how you're evaluated.